Trucking Industry 2026 Outlook

March 2026

Updated March 27, 2026

The trucking industry enters March 2026 at a clearer inflection point than earlier in the year, transitioning from a prolonged downcycle toward a supply-driven tightening phase. Freight demand remains uneven across goods-producing sectors, but rising spot and contract rates, tightening driver availability, and increasing fuel costs are accelerating the rebalancing process. Spot truckload rates remain materially higher year-over-year, and while winter disruptions amplified early-year tightening, current conditions reflect a structurally leaner carrier base and constrained capacity.

OEMs remain disciplined, but orderboards have strengthened further following robust activity through February. Production continues to align closely with backlog rather than speculative growth, reflecting a continued focus on margin preservation. Regulatory visibility around EPA 2027 remains supportive, while additional policy changes affecting driver supply are expected to further constrain capacity. At the same time, higher equipment costs, rising fuel prices, and elevated operating expenses continue to shape cautious fleet investment strategies. As a result, 2026 is increasingly defined as a transition year driven by structural tightening, cost pressures, and selective replacement rather than broad-based expansion.

Freight, Capacity, and Market Balance

Freight volumes enter March 2026 firmer than late-2025 trends suggested, though still uneven across key sectors. While housing and manufacturing remain soft, tightening driver supply, private fleet contraction, and limited fleet expansion are reducing excess capacity more quickly than previously anticipated. Higher diesel prices are also acting as a constraint on effective capacity, reinforcing upward pressure on rates.

The highway Class 8 tractor population continues to contract as sub-replacement build rates, prolonged trade cycles, and fleet exits reshape capacity. Driver supply is tightening at its fastest pace in several years, further limiting available capacity. Tractor inventories are largely normalized following disciplined production cuts, while vocational inventories remain elevated but are gradually improving. Trailer backlogs remain below long-term averages despite recent stabilization, reflecting cautious fleet investment.

ACT Research expects rebalancing to continue through 2026, with firmer rate floors, accelerating contract pricing, and gradually improving supply-demand alignment. While the market has not entered a full recovery phase, structural oversupply conditions have eased meaningfully compared to 2024–2025.

Equipment Markets and Fleet Behavior

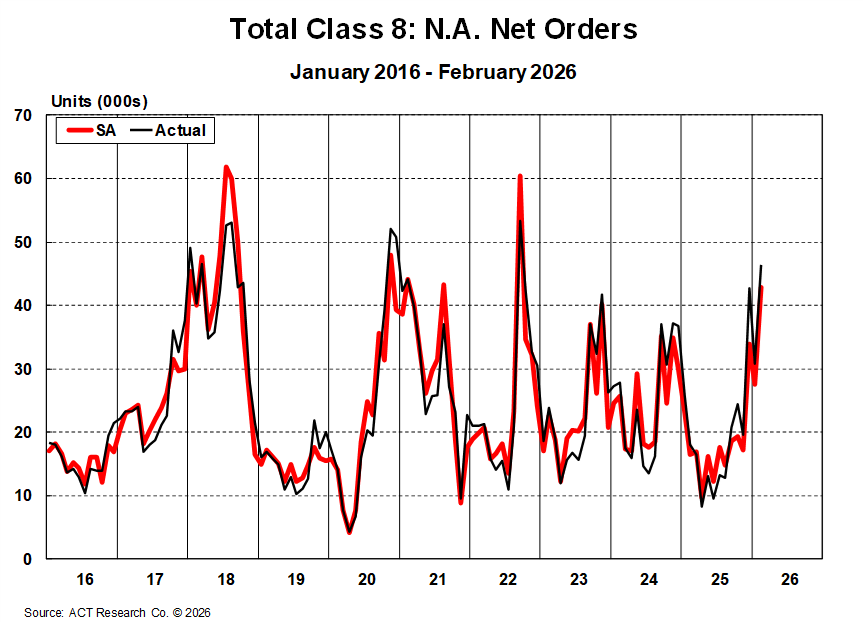

Class 8 production remains disciplined entering March 2026, while order activity has strengthened significantly, with February orders reaching one of the highest levels of the current cycle. Fleet purchasing remains largely replacement-driven, though tightening capacity, stronger rates, and regulatory timing are supporting renewed forward commitments. Elevated equipment costs tied to §232 tariffs, alongside higher fuel, insurance, and financing expenses, continue to moderate expansion-oriented investment.

Medium Duty (Classes 5–7)

Medium-duty markets remain comparatively soft. Orders have improved modestly but continue to track near trend, with limited momentum. Housing- and small-business-sensitive segments remain under pressure, and inventories, while improving, remain elevated relative to long-term norms. Production plans reflect continued OEM caution amid mixed end-market demand.

Trailers

Trailer demand remains in a stabilization phase. While order activity softened in February following earlier improvement, underlying sentiment has improved modestly alongside firmer freight conditions. Refrigerated trailers continue to show relative strength, dry van demand is stabilizing, and flatbed demand remains tied to uneven industrial activity. OEM build plans remain disciplined as manufacturers prioritize backlog alignment and inventory control.

Regulatory and Cost Environment

Regulatory clarity remains improved entering March 2026. EPA’s 2027 framework is better defined, while additional policy changes impacting driver eligibility are expected to further constrain labor supply over time. While core emissions requirements remain intact, reduced uncertainty is supporting fleet planning and contributing to early prebuy discussions.

Tariffs remain embedded in equipment pricing. §232 heavy-vehicle tariffs continue to elevate acquisition costs, while rising diesel prices, higher interest rates, insurance premiums, and compliance costs are increasing total cost of ownership. These combined pressures are reinforcing disciplined capital allocation and limiting near-term capacity expansion.

Zero-emission adoption continues in targeted applications such as drayage, urban delivery, and utility fleets, though broader adoption remains constrained by cost, infrastructure readiness, and policy variability.

Outlook for 2026

The trucking industry is not yet in a full recovery phase—but it is now firmly transitioning out of the oversupply conditions that defined the prior two years. Capacity contraction is accelerating, driver availability is tightening, and both spot and contract rate floors are resetting higher.

Freight demand remains uneven across industrial and housing-linked segments, but improving supply-side alignment and rising cost pressures are creating a firmer operating environment. ACT Research now views 2026 as a supply-driven transition year—characterized by tightening capacity, improving pricing dynamics, and gradual margin recovery. A durable recovery will depend not on a sharp surge in demand, but on sustained capacity discipline, stabilization in operating costs, and continued rate normalization across the truckload ecosystem.

Stay Ahead with Smarter Freight Insights

Success in trucking and freight comes from knowing what’s next—not just what’s now. At ACT Research, we deliver forward-looking market intelligence that helps you anticipate shifts, prepare for cycles, and stay strategically positioned. As your trusted transportation intelligence partner, we give you the tools to act with confidence—so you can optimize operations, reduce risk, and drive stronger profitability.